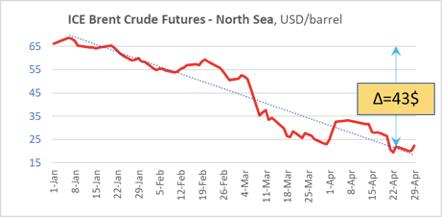

Since late 2019 there has been a tendency of lower crude oil prices on the global market. However, on March 9 at London Intercontinental Exchange Brent Crude Futures – North Sea – Wave went down $12 to $35.45/barrel. Brent lost 25,5%. The market crashed and impacted all spheres of life undermining economic activity in the entire world. How did this situation affect the EaP region?

Where Does the Crisis Come from?

The oil market crisis is a result of many processes. The amount of crude oil present on the market was increasing, first and foremost, due to more mining in the USA. The end of 2019 saw the USA mining more crude oil in 24 hours than Saudi Arabia and Russia. The USA became global exporters of oil and gas leaving import at the minimal level. At the same time, there was a process of reducing global oil demand. Already in 2019 global oil consumption went down against 2018. This tendency was further reinforced by introducing restrictions and lowering business activity as a result of the COVID-19 pandemic. For instance, in January 2020 China’s import of Russian oil dropped by 30% against the same period last year.

Fig. Intercontinental exchange London / 2020 / oil price dynamics. Source: ICE

However, there is a direct crisis accelerator, namely the broken negotiations on prolongation of OPEC+ agreement in March, which led to reduced limitations on crude oil mining. In April these processes deepened. New agreements on reduced mining did not save the situation. The process can be characterized by negative WTI crude oil prices at NYMEX and Urals in April. Prices went drastically down and became negative largely due to stock market speculations, weak demand and the lack of storage facilities. Yet at the same time negative prices (seller pays buyer) are indicators for the crisis depth.

Russia’s Changing Behavior

It is yet difficult to make a forecast regarding the crisis aftermath and its impact on life. Much will depend on containment measures and countermeasures implemented all over the world. The IMF and its World Economic Outlook (April 2020) report that 2020 global growth will decrease minus 3% after global economic growth rate of 2.9% in 2019. Gross Domestic Product is expected to go down in most European countries, EU in general (-7.1%) and in all six EaP countries. Russia’s economy will go down 5.5%, while as early as March OPEC reported 0.5%. Moreover, forecasts underline that there are risks of even deeper economic recession.

These facts highlight the scale of such issues. In the Russian Federation that is highly dependent on hydrocarbon export, a so-called “working version” of 2020 federal budget forecast has recently been developed. It is based on supposed crude oil price of $20/barrel. In this case federal budget deficit will make up approximately $75 bn and it is planned to be covered by funds of the Russian Federal Wealth Fund. However, how long this money will last is yet to be discovered.

“The current crisis is changing Russian behavior and encourages it to come to compromises with its neighbors”

It seems that the current crisis is changing Russian behavior and encourages it to come to compromises with its neighbors. For instance, Belarus, while getting most of its crude oil and gas via its eastern border, yet again faced the issue of its main neighbor freezing crude oil supplies early this year. Experts believed then that such Russian actions mean more pressure on Minsk during deeper integration negotiations between the states. Such a break in crude oil supplies meant a threat of freezing Belarusian refinery industry, however, it also demonstrated the importance of solidarity and the need for better infrastructural contingency between EaP countries.

Already on March 12 the first tanker with Azeri Light of 90 thousand tons arrived in Yuzhny offshore oil terminal. JSC Ukrtransnafta accepted crude oil and transported it via Odessa-Brody pipeline and one of the two trunk lines of Druzhba (Friendship) pipelines directing it to Belarusian oil refineries. Therefore, the route from oil fields in Azerbaijan via Black Sea ports (Georgian Supsa and Ukrainian Yuzhny) and pipelines Odessa-Brody-Mozyr started to function, thus allowing Azerbaijan oil Azeri supplies to Belarusian oil refineries and launching their work. This was not the first instance of Belarus pumping oil via Odessa-Brody pipeline: in 2010-2012 this route was used for pumping crude oil from Venezuela.

It is worth noting that already in several days, in late March Rosneft changed its position and agreed to restart crude oil supplies to Belarus. The reason for restarting the supplies is unknown. However, market conditions were surely favorable. Moreover, Brent crude oil futures did not exceed $26-27/barrel in late March. As for Russian crude oil Urals, its March average price made up $29/barrel (official statistics of RF Ministry of Finance), while physical deliveries were even cheaper. For instance, on March 30, Urals barrel dropped to $13 in Rotterdam.

Time to Make Stocks

The impact of global oil crisis also mainstreamed other issues of energy security, in particular, the necessity to maintain minimal stocks of crude oil and petroleum products. EU association agreements as well as Energy Community membership oblige Ukraine, Georgia and Moldova gradually implement EU energy legislation regarding maintaining minimal stocks of crude oil and petroleum products (Directive 2009/119 /EU).

Each country must ensure that the total oil stocks maintained at all times within the Community for their benefit correspond, at the very least, to 90 days of average daily net imports or 61 days of average daily inland consumption (Article 3) and additionally 10% of stocks (technically inaccessible) of all types of products. There is a regulation that at least one-third of stocks should contain petroleum products. There is also a requirement to develop an action plan in case of emergency that would be reflected and approved in the special Plan.

“Given the conditions of low global oil prices EaP countries need to mobilize their work in order to create national stocks of crude oil and petroleum products”

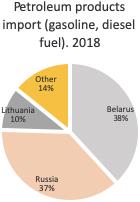

Fulfilling minimal stock obligations is also essential taking into account energy security. In all EaP countries except Azerbaijan crude oil and petroleum products are mostly imported. Ukraine annually spends several billion dollars to solve this issue. According to State Statistics Service of Ukraine, in 2018 8.06 ml tons of petroleum products were imported to the country, equivalent to $5.5 bn dollars. Imported petroleum products make up 73-80% of total consumption. Georgia, Moldova and Armenia do not have their own refineries and therefore import 100% of petroleum products, with most of the import coming from the Russian Federation, the aggressor state.

Oil crisis is a great opportunity to make stocks while saving money. For example, calculations aided by EU in 2018 demonstrated that Ukraine’s minimal stocks should consist of 25-30% of crude oil and 70% of petroleum products (38% of motor petrol and 62% of diesel fuel). The total volume of necessary 90-day 24-hour average import is calculated in oil equivalent at the level of over 2 ml tons including 1,4 ml tons of petroleum products. Let us remember that Brent average annual crude oil price made up $72/barrel (approximately $514/ton). Therefore, to create stocks under current conditions will cost less, saving some hundreds of million dollars.

The importance of stock issue is further highlighted by Energy Community Secretariat. According to it, as of November 2019, legislative obligations on minimum stocks are not completely fulfilled in EaP countries. For instance, in Georgia and Moldova the general implementation indicator is only 8%, while solutions for such issues as lack of storage capacities are yet to be found. Already in 2018 a special draft bill on creating minimal stocks was introduced in Ukraine and it has to be directed to the Verkhovna Rada of Ukraine as soon as possible.

It is obvious that given the conditions of low global oil prices Ukraine and other EaP countries need to mobilize their work including amendments to legislation in order to create national stocks of crude oil and petroleum products.

Lower global prices may also have a positive economic impact. Given the conditions of lacking storage capacities Ukrainian Naftogaz is working on attracting oil suppliers and providing them with oil storage services. Such services have an estimated monthly profit of $1-3 ml. The preparation includes developing a “customs warehouse” mode based on oil storage capacities (V = 1,083 ml cubic meters only in Ukrtransnafta). Such a mode provides for an opportunity not to pay VAT while importing raw stuff in order to encourage suppliers. Gas “customs warehouse” has been operating for two years already, which in 2019 allowed to provide European companies with storage services of 24 bn cubic meters of gas in Ukrainian gas storage facilities and plan additional 5-6 bn cubic meters for 2020.

EaP is a Winner. Almost.

One of the Eastern Partnership goals is providing for contingency of gas, oil and other energy infrastructure. Recent crisis situations only support this idea and further prioritize this goal, while the fast track of Azerbaijani oil supplied using Georgian and Ukrainian infrastructure demonstrated obvious advantages for everyone. In general, it seems likely that the oil crisis played into the hands of import-dependent countries in the region.

Serious financial losses within EaP will be relevant in case of Azerbaijan that is a large oil producer, having produced 37.5 mln tons of oil and 35.7 bn cubic meters of gas in 2019. Oil and gas export of hydrocarbons is extremely important for developing domestic economy. The results of 9 months in 2019 show that oil export made up 75,76% from the entire Azerbaijani export. According to the State Customs Committee, within the period of January-September 2019 Azerbaijan exported 23,3 ml tons of oil that made up some $11,267 bn.

Armenia does not have its own oil and gas resources and is completely dependent on foreign supplies. Petroleum products are mostly imported from the Russian Federation. In 2018 330 thousand tons equal to $278 ml at the world price of $71.9 per barrel were imported. Therefore, there are preconditions that Armenia will spend significantly less resources in order to import petroleum products. As for gas that is now supplied by Gasprom and is a kind of monopoly, the Russian Federation does not agree to cut the prices as was voiced on April 22, on the tribune of Armenian parliament.

Belarus has a strong oil refining industry and exports significant volumes of petroleum products while importing the complete amount of crude oil needed for its refining capacities. The termination of crude oil supplies from the Russian Federation early this year resulted in boosting deeper relations with EaP partners and diversifying sources and routes of crude oil supplies. Moreover, global oil crisis facilitated negotiating a good deal with the Russian Federation and it looks like it is beneficial for Belarusian interests.

Georgia also does not have its own crude oil mining and completely depends on import. Lower crude oil prices will lead to reduced cost of petroleum products import. Yet the coronavirus pandemic has a negative impact on economic activity and transportation resulting in lower oil product consumption that went down 40% in March. Moreover, possibly aggravating economies in countries mining crude oil may have a negative impact on Georgia’s export and the country’s economy in general. However, low prices also mean a good opportunity to create national stocks of crude oil and petroleum products, which will increase the country’s energy security and sustainability.

Moldova imports petroleum products thus satisfying its own need. Therefore, lower global prices should make a positive impact on its economy. Yet natural gas is supplied by Russian Gazprom at the price ($174/1000 cubic meters) that is significantly higher than the price at the European market and it has not been revisited yet. New agreements between Transmission System Operators of Ukraine and Moldova provide an opportunity to purchase gas in the European Union and supply it to Moldova at low prices and diversify sources and routes of gas supplies. Low oil prices mean a good time for making stocks in accordance with EU Directive requirements.

Ukraine does have oil and gas mining, however, it imports the larger part of petroleum products and therefore, should feel the positive impact of lower global oil prices. It is likely that there will be certain difficulties for mining enterprises. This period also gives a chance to create national stocks of petrol and diesel fuel and provide services of storing crude oil and gas to European companies. The situation at the European market facilitates efficient use of oil pipes, oil reservoirs and underground gas storages. The record amount of gas remains in EU UGSF and adequate pricing creates favorable conditions for providing gas storage services to European companies. Oil crisis mainstreams the necessity of restoring oil refining capacities in Ukraine.

Fig. Import of petroleum products to Ukraine. Source of information: SFS.gov.ua

Moreover, EaP countries aim to develop relations with other European countries. Ukraine, Moldova and Georgia are full members of the Energy Community and are deepening their relations with the European Union according to the conditions provided by Association Agreement. Implementing European energy legislation should as a result allow them to become full members of EU gas and energy markets.

It is worth reminding that the eleventh Annual Assembly of EaP Civil Society Forum in last year’s declaration (December 2019) turned to EU (p. ІХ) calling on it to support aspirations to become full members of EU gas market that will connect member states and three EaP countries. Full membership in EU single market will allow for better coordinated plans and strategies, as well as facing energy security threats together. This also concerns challenges caused by oil crisis and the virus pandemic. Their impact should be addressed within the all-European context.

Conclusions

- Global oil market crisis and the virus pandemic are serious challenges for the world, EU and all six EaP countries. Facing energy challenges should be consolidated taking into account all-European positions.

- Involving energy infrastructure of four EaP countries as route components for Azerbaijani oil supplies to Belarus yet again highlights the importance of contingency for gas and oil infrastructure within the EU and its neighbors in order to boost energy security.

- Integrating into EU energy market, boosting coordination strategies and infrastructure plans will provide for minimizing negative aftermath and getting advantages such as better security for supplying gas and other hydrocarbons.

- Oil market pricing opens a window of opportunity for a faster minimal crude oil and petroleum products stocks according to the EU oil Directive.